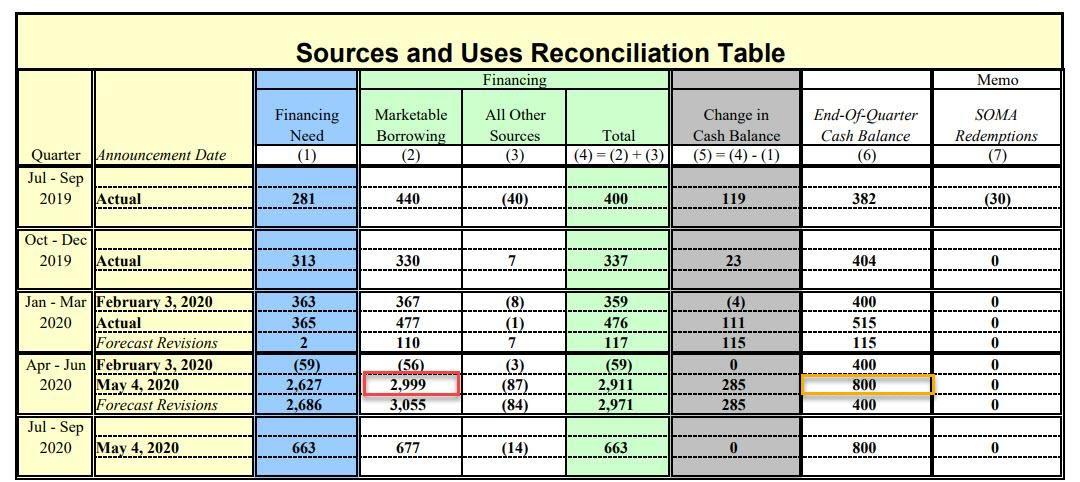

Back on May 4, in its then-latest estimate of Marketable Borrowings the US Treasury shocked markets when it unveiled that in the April-June quarter it would borrow a humongous $2.999 trillion, exponentially higher than what it had expected to borrow during the quarter in its previous estimate in February when it forecast a $56 billion decline in debt. And while the projected debt number stunned the market, it barely registered on the price or yield of US Treasurys for the simple reason that just weeks earlier the Fed announced it would monetize all gross debt issuance for the US when it unveiled Unlimited QE, something it has been doing since.

This massive surge in debt issuance would also result in a far higher Treasury cash balance which would be used to pre-fund various fiscal stimulus programs, and as the chart below shows, that's precisely what happened with the Treasury cash balance exploding from $400BN at the end of March to an record high just above $1.7 trillion currently, an amount that is just waiting to be spent as soon as Congress gives the green light.

In retrospect the cash surge was too much: in fact, more than double what the Treasury had expected on May 4. While the Treasury had forecast a $3 trillion increase in marketable borrowing for the quarter ending June 30, it also expected the cash balance to grow to $800 billion on that same date (shown highlighted in yellow on the table below).

And yet the final number ended up being approximately $900 billion higher, meaning that the Treasury had substantially overshot its funding need and suddenly found itself with a record cash buffer.

So with all this extra cash in hand, did the Treasury reduce its debt needs? As shown above, five months ago the Treasury expected that it would need to borrow $677BN in the final fiscal quarter of the year ending Sept 30, which while a massive number, was still well below the $2.753 trillion it ended up borrowing (just shy of the $2.999 trillion initial forecast, a number which was not hit due to "lower-than-projected expenditures and higher receipts largely offset by the increase in the cash balance.")?

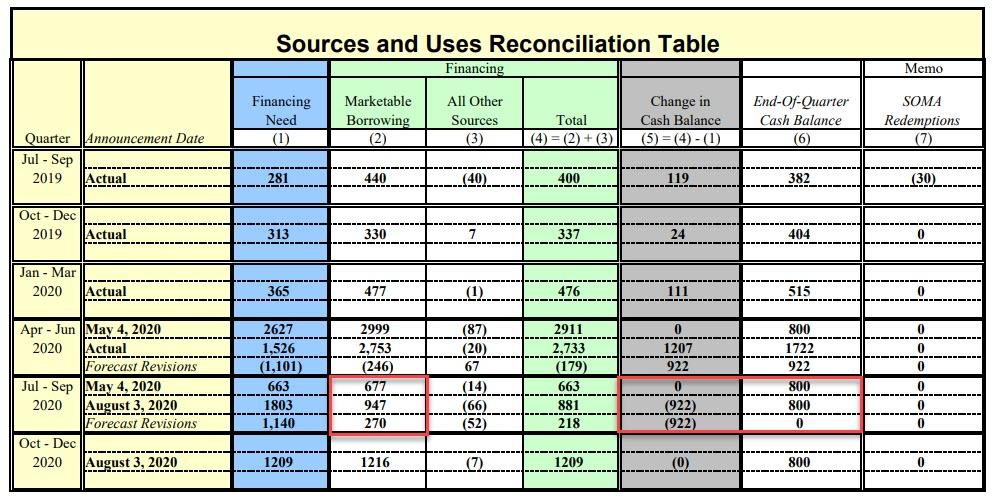

The answer, as we pointed out in August, was a resounding no because as it disclosed in its latest estimate of Marketable Borrowing needs, the Treasury once again surprised markets by announcing it would borrow a whopping $947BN last quarter, $270BN more than it had forecast a quarter ago, even though the Treasury started this quarter with a cash balance that is $922 billion higher than it had expected one quarter ago!

Why this unexpected increase in debt even though the Treasury was starting off with nearly $1 trillion more in cash than originally budgeted? This is how it explains it.

During the July - September 2020 quarter, Treasury expects to borrow $947 billion in privately-held net marketable debt, assuming an end-of-September cash balance of $800 billion. The borrowing estimate is $270 billion higher than announced in May 2020. The increase in privately-held net marketable borrowing is primarily driven by higher expenditures, due to a shift from the prior quarter and anticipated new legislation, largely offset by the higher beginning-of-July cash balance and higher receipts.

In other words, not only will the Treasury draw down on $922 billion in cash in the calendar quarter the ends in less than two months...

... but it will also sell enough debt to raise an additional $881 billion (net) which will also end up being spent, suggesting that in the current quarter the Treasury plans on spending a gargantuan $1.8 trillion, something which as we learned last week was the latest Trump offer to Pelosi and House Democrats (an offer which Pelosi just turned down earlier today).

But that's not all, because in its first glimpse of the current Oct-Dec quarter's funding needs, the Treasury now expects to borrow another $1.216 trillion in privately-held net marketable debt, once again assuming that the end-of-December cash balance remains unchanged from the Sept 30 balance of $800 billion. This means that the Treasury will spend an additional $1.2 trillion in the quarter ending Dec. 31, assuming every dollar it raises in the open market is then promptly spent (since the cash balance remains unchanged).

According to the Treasury, "these estimates assume $1 trillion of additional borrowing need in anticipation of additional legislation being passed in response to the COVID-19 outbreak."

So what does this mean?

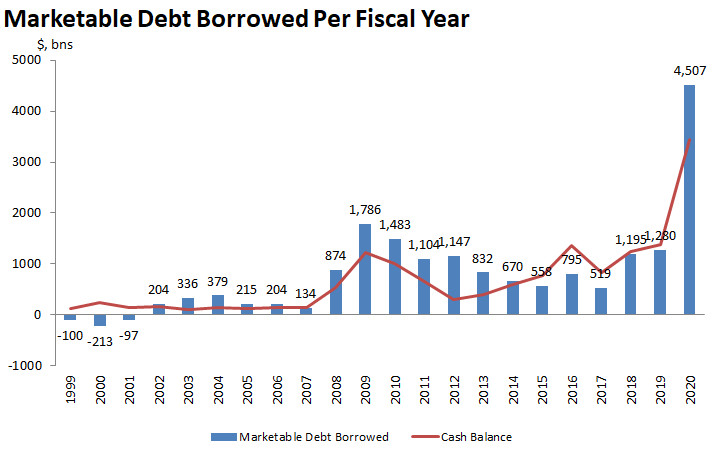

First, when putting together the actual data for the first three quarters of fiscal 2020 and adding the Fiscal Q4 estimate of $947BN in new issuance, the Treasury will borrow a record $4.5 trillion in Fiscal 2020, more than it borrowed in the previous view years combined!

Second, it means that for calendar Q3 and Q4, the Treasury planned on spending almost $3 trillion consisting of:

i) a drawdown in cash from $1722 billion to $800 billion, for $922 billion, in the quarter ending Sept 30

ii) new debt issuance of $947 billion in the same quarter and

iii) new debt issuance of $1,216 billion in the quarter ended Dec 31

... for a grand total of $3.085 trillion in new funds (either from spending cash or raising debt).

And even if the Treasury uses some of this cash to pay down maturing Bills (which we doubt as it will most likely keep rolling this short-term debt indefinitely with rates at all time lows), it means that as recently as August, the Treasury was budgeting for nearly $3 trillion for Congress and Trump to spend as they fit in order to boost the economy to ensure that there is no "double dip" economic crash. It also meant that for all the posturing about whether the $1 trillion Republican or $3 trillion Democrat stimulus package is accepted, the Treasury was already budgeting for the latter.

* * *

Alas, a problem emerged: with less than 4 weeks left until the elections, Congress and Trump remain hopelessly deadlocked on when - and if - a new stimulus will take place. And while that in itself is a major problem for an economy and for Trump's re-election chances (which explains why Democrats are playing hardball on a new deal and will only accept it if it includes bailouts of insolvent state pensions in Democratic states), something we explained two weeks ago, "Failure To Launch New Fiscal Stimulus Would Have Catastrophic Consequences For The US Economy", another major problem has emerged.

The growing uncertainty over a new, fifth fiscal deal raise significant questions about the Treasury’s plans for managing its cash balance - which as shown above, is at $1.69 trillion and remains more than double its projected target of $800 billion at Dec 31 - between now and year end.

So, as BofA first hinted last week, if no deal is reached this quarter, the Treasury would need to pay down nearly $1 trillion worth of bills in the next two months to reach its year-end cash target of $800BN, writes Barclays strategist Joseph Abate.

And yet, another fiscal stimulus deal remains just a matter of time, the only question is whether before the election, or after. That however is a key wildcard for the massive cash holdings at the Treasury, which Trump was hoping to use up before the election and prop up the economy.

Indeed, as Abate writes, a spending package is still likely in the new year, and since "the purpose of the Treasury’s cash stockpile was to have immediately available resources to finance a portion of any new stimulus, we see no reason for the Treasury to cut bill issuance aggressively this quarter."

Moreover, the decline in bill rates over the summer means the Treasury may have a harder time selling large amount of bills next year. "This may be an additional reason why the Treasury has not decided to pay down bills or run down its cash balance in case it would be forced back into the bill market," according to Abate.

For its part, Barclays expects the Treasury will flag a one-year note linked to SOFR at the November refunding announcement, with the first sale delayed until February. The Treasury will probably need to trim bill issuance to make room for the new note, in addition to any potential supply changes created by a stimulus package.

Maybe, but there's more: as BofA rates strategist Marc Cabana wrote last week, the Treasury will ultimately target a $400BN cash balance after stimulus needs are met & PPP loan forgiveness is complete, suggesting a $1.2 trillion drawdown from current cash levels. Making matters worse, and why the Treasury could face material pressure to get their cash balance even lower by the summer of next year is that the Treasury will need to lower their cash balance to $133BN by end July ’21 to be in compliance with the existing debt limit law (the 2019 Bi-Partisan Budget Act suspended the debt limit through end July ’21 but when the debt limit is reinstated UST needs to hold no more cash on hand vs when the bill was originally signed into law which is $133BN).

As a result, if a new debt ceiling is not instituted before end July ’21 - due to continued Congressional bickering for example - it could imply less financing need from bills, all else equal. The impact of different TGA levels on expected Q420 and 1H21 net bill supply in tables 3 and 4.

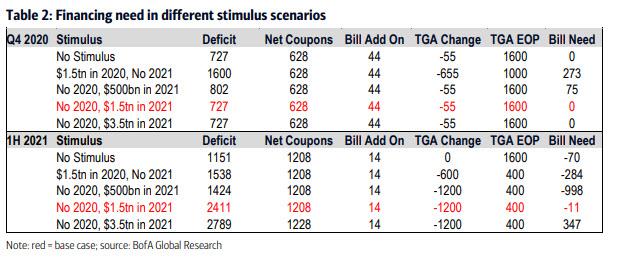

What all of this boils down to, simply said, is that depending on the trajectory of stimulus discussions, the Treasury could see vast swings in its cash balance which in turn would affect its Bill financing strategy. As we discussed last week, there is a range of bill supply outcomes between now & 1H ’21 as shown in Table 2. Much of the bill supply impact will be a function of the Treasury cash balance level, which remains near record levels. The implications of a few bill supply scenarios are listed below:

Pre-election stimulus: In Q4 ’20 bill supply would likely total $250-$300BN. The Treasury will drop their cash balance to $1TN, which would add ~$600BN of cash into the banking system. The expected increase in banking system cash would likely overwhelm bill supply & keep front end rates stable to lower.

Base case (no stimulus pre-election, $1.5tn post inauguration): In Q4 ’20 bill supply will likely be flat or slightly negative with a Treasury cash balance at year-end of $1.6tn. This is lower vs prior forecasts due to a downward revision in deficit estimates and the TGA ending September higher than BofA had previously anticipated. In 1H ’21 bill supply will also likely be flat on net but there may be one notable variation; Cabana "might anticipate" $200-$300BN bill supply after stimulus is passed in Feb or March but expect this would be paid down after the April tax date. The decline in Treasury cash balance will limit the need for elevated bill supply.

Extreme scenarios: in 1H ’21 a “supersized” or “skinny” deal could see bill supply range from positive $350-$400BN to negative $1TN. In a “supersized” scenario the bill supply increase would likely be greatest after a bill is passed in Feb or March ’21. In a “skinny” deal the risk of sharply negative bill supply stems from a potential “forced” reduction of the Treasury cash balance.

The bottom line is that depending on the outcome of the ongoing stimulus discussions, the Treasury may end up injecting approximately $600 billion of cash into the banking system as existing Bills mature and are not rolled over, which according to Cabana "would likely overwhelm bill supply & keep front end rates stable to lower." It would also mean that banks suddenly have to allocate a massive amount of excess cash into various securities, which if previous instances of such capital reallocation inflection points are an indicator, would - together with the Fed's ongoing injection of at least $120BN in reserves each month courtesy of QE - result in a wholesale meltup across the entire risk spectrum.

The irony of all this is that should there be no fiscal deal, and should Trump lose the election, the market may end up exploding higher in the last weeks of the year... just as the US economy - starved for more stimulus capital - careens into a double dip depression.