The U.S. natural gas pipeline sector is entering a challenging period for recontracting a major chunk of its capacity. The numerous pipeline systems built during the early years of the Shale Era’s midstream boom were anchored by 10-year, firm shipper contracts, mostly with producers, making them so-called “supply-push” pipelines. Many of those initial contract periods have begun to roll off, exposing pipelines to producer-shippers’ renewal decisions based on current fundamentals. Shippers typically expect substantially lower rates for a renewal contract, because much of the pipeline has been paid off through depreciation. But there’s another issue that is becoming more important: shipper recontracting may not happen for market reasons. For pipeline owners, this is happening at the worst possible time. The market is in turmoil and facing ongoing uncertainty. Gas production is down, demand from LNG export facilities is in flux, and regional supply-demand dynamics are shifting. As if that weren’t enough, new, large-diameter pipelines out of the Permian now nearing completion will reshuffle gas flows around the country. And other transportation corridors that not long ago were bursting at the seams and feverishly expanding to ease constraints are now at risk of being underutilized. Today, we discuss the factors that together may present significant risk for pipelines approaching the proverbial recontracting “cliff.”

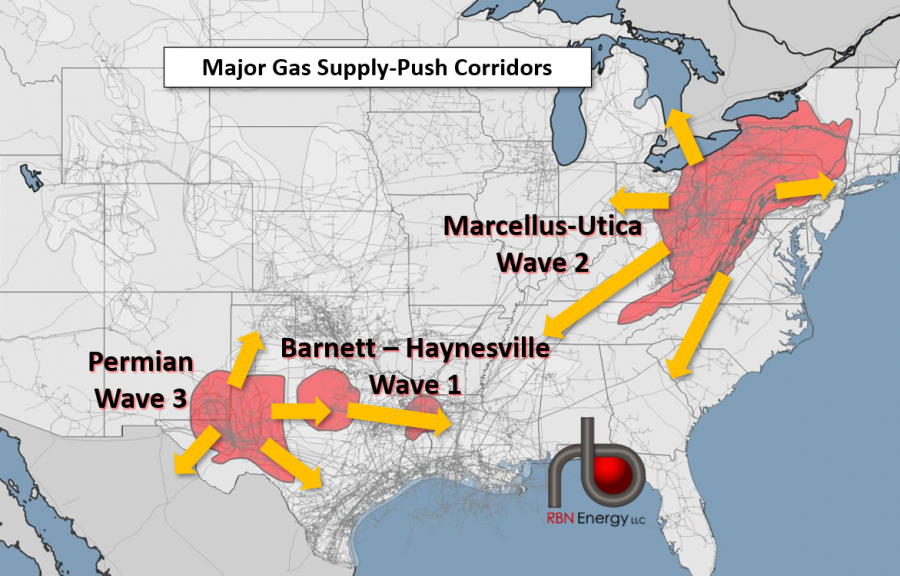

The Shale Revolution began in the early 2000s and quickly ramped up production in several regions, one after another. Figure 1 shows the three plays that have resulted in the biggest capital investments in supply-push pipelines for natural gas: Barnett/Haynesville, Marcellus/Utica, and Permian. Other plays such as Bakken and SCOOP-STACK also ramped up, but didn’t result in the huge waves of infrastructure development that happened in these three areas.

Figure 1. Major Supply-Push Corridors for Shale Gas. Source: RBN

It started with the Wave 1 pipelines out of the earliest shale play, the Barnett Shale in North Texas, then expanded to the Haynesville in East Texas and western Louisiana, which became the dominant driver of growth. Then, Wave 2 was driven by the enormous expansion of production out of the Northeast plays, Marcellus and Utica. For decades, the Northeast had been piping in the bulk of its gas supply from the far-away Gulf Coast. The huge production gains quickly filled the needs of the Northeast consuming market, and then reached levels that needed to be shipped out of the region. The existing gas pipeline infrastructure was way short of adequate for these outflows, spurring a slew of reversals, expansions, extensions, and brand-new pipelines in five different directions — a topic we’ve blogged about many times since back in 2012, when we posted The Marcellus Changes Everything (our forecast back then of almost 16 Bcf/d by 2016 seems quaint in hindsight), to our most recent You’ve Got Your Troubles blog. Most of these projects shared a common trait that had rarely been seen in the pre-shale decades: they were “supply-push” projects, mostly supported by transportation contracts with producers, rather than utilities and other gas consumers, because it was the producers who did not want their supply to be trapped behind severe pipeline constraints and subject to the resultant pressure on prices. So a brand-new generation of pipelines funded by producers seeking to ensure takeaway capacity became the enabling matrix that allowed shale production to grow and mature.

Then, most recently, the Permian Basin, with its massive associated gas volumes tagging along with oil production, has resulted in Wave 3. Again, producer-shippers are looking to get pipe capacity to different destination markets, although mostly they’re headed to the Gulf Coast for export.

Most of the transportation contracts in Waves 1 and 2 had terms of 10 years — the same is true of the Permian, but its infrastructure growth is younger, so these pipes are not yet facing the recontracting cliff. Ten-year firm transportation (FT) contracts don’t just underpin pipeline investment; they serve as the primary indication of need for the pipeline at the Federal Energy Regulatory Commission (FERC), the agency that has to decide whether to let the pipeline be built or expanded, at least for the interstates, which make up almost all of the pipes in Waves 1 and 2. So it’s fair to say that these decade-long producer commitments underwrote the gas infrastructure buildout. A natural consequence of these contracts was that for 10 years, the producers — not the pipelines — were taking the full market risk that firm capacity would be needed on the chosen routes. That was good then, but it’s been 10 years, or at least it’s about to be, for most of those pipelines, and a lot of things have changed. What happens next?

The appeal of paying firm monthly reservation charges to transport gas from Point A to Point B appears to have faded or even disappeared in many markets in the intervening years. There are lots of reasons for that, depending on which market we are talking about. For example, the concentration of supply growth may have moved (from offshore/Rockies to the shale basins); the targeted demand markets may have changed (U.S. power generation to LNG exports); or the pipeline simply might be too big for the supply that wants to go through it (Barnett/Haynesville, Permian, and possibly other markets).

Regardless of the reason, the outcome is the same: the regional natural gas price differential between A and B drops to a level lower, sometimes significantly lower, than the cost of moving gas from A to B. Why does this happen? How does a pipeline built to protect a producer from the possibility of a wide differential between the producing basin (“A”) and the destination market (“B”) end up out of the money? There are two ways, one as old as time and kind of obvious, the other a symptom of how fast the boom in shale production came on.

The old-and-obvious reason for a pipeline to be built that ultimately proves too big for its market is that once a pipeline eliminates a bottleneck, getting across the constraint isn’t worth as much — the bottleneck is relieved by the very pipeline that sought to capitalize on it. Unless production growth by the end of the initial contract period exceeds the expanded pipeline capacity and leads to another logjam, the producer-shippers don’t have the incentive to pay the reservation charges for as much (or any) firm space after their initial long-term contracts expire; they can just rely on pay-as-you-flow interruptible transportation (IT) service. This is what happened to the entire offshore Gulf of Mexico, where even purportedly firm contracts now allow shippers to reduce their contract levels as production declines. In this case, a pipeline’s “firm” service is not based on reservation charges at all, but only on volumetric charges as gas actually goes through the meter. And, for the most part, the region’s major systems are completely characterized by interruptible-only service.

The more recent cause for some supply-push pipelines being too big for their markets stems from producers signing up for and underwriting capacity that ended up exceeding available production volumes. Underwriting new firm pipeline capacity was a pretty new thing for most producers, and the Shale Revolution leapt into high-volume existence in a very short period of time. So the producers projected significant future production growth and definitely wanted to avoid getting trapped behind a bottleneck. As a result, they sized their commitments based on production that, in a number of cases, never reached the projected levels as prices dropped and their supplies were unable to compete with lower-cost plays. This situation really highlights the difference between a projection, where you figure out what you think is going to happen, and a commitment, where you have to pay money for 10 years, regardless of how things work out. Put very simply, several pipelines were built that were big enough to handle a lot more production than ever happened. When the original 10-year commitments ran out, producers had the benefit of overbuilt capacity, with no need to pay a premium to use it, or to make a firm commitment to it.

So if either of these scenarios plays out, a pipeline may face the prospect of being “stranded” if it cannot renew current contracts or find replacement shippers. In other words, it would be left with more capacity available than shippers will pay for at the original contract rates. The upside of pipeline transportation is that it is almost always the only way to economically transport natural gas over land. The downside is that big pipelines are impossible to relocate. There certainly are some pipeline routes — particularly on the north-to-south routes out of the Marcellus/Utica — that should see production growing enough to push the need for new capacity such that, as contracts roll off, it’s worth the producer-shipper’s while to hang onto the capacity. In those cases, contract renewals are really only limited by the creditworthiness of the renewed or replacement shippers (unfortunately, not a small risk these days, as producers have been hammered financially.) But generally speaking, pipelines facing recontracting are in a precarious position.

As pipelines assess recontracting risk, and as new investors observe the fate of the supply-push pipelines reaching the end of their contracts, it’s important to note that supply-push pipelines are almost exclusively funded by “negotiated rates,” i.e., non-tariff rates that do not allow the pipeline to raise rates if load is lost. This is different than for a lot of older, demand-driven systems, which charge tariff rates that can be adjusted as things change. So supply-push pipelines face a special kind of risk that is good for shippers but bad for the pipelines. Most supply-push pipelines are also stand-alone, even if built as part of a large, complicated system like Texas Eastern Transmission (TETCO) or Transcontinental Gas Pipeline (Transco). That means that their costs and revenues are split out, or treated “incrementally,” so they can’t be subsidized by raising rates to other shippers. In short, a supply-driven pipeline is on its own if shippers start disappearing.

Does this mean that a lot of pipelines will be stuck as their contracts expire, unable to convince anyone to sign up for firm service? How does recontracting risk look around the country? What can a pipeline do if its origin and destination combinations are less attractive than they were when it was built? Are there major differences in the size of the risk or the reasons for the risk? And what effect could the outcome have on new pipeline investment?

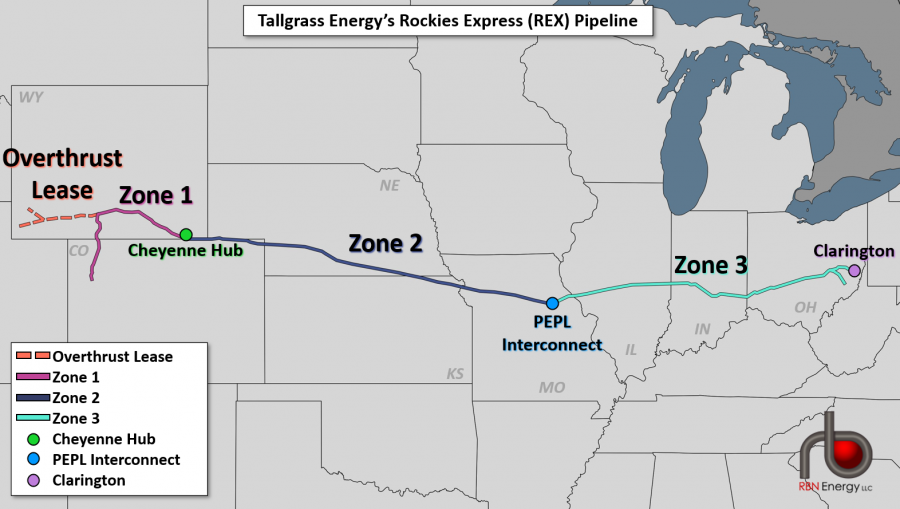

To begin to answer those questions, here and in subsequent installments of this story, we’ll look at some examples of supply-driven pipelines confronting the “moving supply/moving market,” “lack of bottleneck,” or “oversized in the first place” dilemmas. A large, classic example of supplies and markets moving around that has already happened and been resolved is Rockies Express, or REX, shown in Figure 2.

Figure 2. Rockies Express (REX) Pipeline. Source: RBN

REX was one of the first big supply-driven pipeline projects built more than a decade ago, and one we’ve covered extensively in our daily blogs (most recently in I’ll Take You There), but the story is still pertinent here. REX was built to let Rocky Mountain gas get all the way into Ohio and connect with the East Coast pipeline grid in order to serve what were at the time high-priced Northeast markets. But by the time it came online in 2009, the shale boom was happening and the fastest-growing supply area in the nation — Marcellus — was at the delivery end of REX. When your business is carrying gas from Point A to Point B, finding out there is an abundance of gas already at Point B is an unfortunate development. The anchor shippers had taken on the risk that something like this might happen by committing for 10 years, but now their gas was only welcome in a much lower-priced Midwestern market on the way to the Northeast. So REX faced a very uncertain world when the anchor contracts ran out in 2019.

REX’s primary owner, Tallgrass Energy, responded to this challenge by signing most of its shippers back up at rates that recognized the lower value of only needing to get to the Midwest. (We detailed those recontracting deals in our Express Yourself blog series.) But before that, they also had taken the bold step of converting the pipeline’s eastern segment (Zone 3 in Figure 2 map) to two-way or bidirectional flow. Once it had the necessary approvals to allow westbound flow, REX invested new capital to attract Marcellus and Utica gas to also go to the Midwest, albeit from the other direction. So REX has been able to adapt to market shifts and avoid becoming a “pipe to nowhere.” The lesson? Be very flexible, and recognize that the value of a pipeline’s capacity may drop and need much lower rates after the expiration of the primary contracts, so it had better make it up in volume.

But where REX found success, other pipeline corridors around the U.S. may face new dilemmas. In upcoming blogs, we’ll look at the examples of the north-to-south pipelines out of Appalachia that cured outbound bottlenecks and, as discussed above, flesh out whether supplies could catch up prior to their contracts’ expiration. We’ll also review the Permian situation where new capacity will soon outpace volume growth and what lessons pipelines in that region might learn from the Barnett/Haynesville market. The recontracting situation varies widely around the country.

The bottom line is that everything in the market is in flux, and all the pipelines are physically static, so they have to find more and more ways — as REX did — to provide services that address the market’s changing needs. Dealing with the issue takes a deep understanding of both the commercial and the regulatory dynamics going on now and anticipated over the next several years, as well as a lot of creativity.

RBN’s Oil and Gas Advisory Services specialize in helping clients navigate issues surrounding pipeline rates, recontracting, strategy, and litigation. Click here for more information.

"I Don't Know Where I'm Bound" was written by Terry Cuddy and Johnny Cash, and appears as the third song on the 2000 re-issue bonus CD of Johnny Cash at San Quentin, Cash's 31st album. The song lyrics were written by an inmate at San Quentin (Terry Cuddy), and presented to Cash the day before he performed there. Cash wrote the music to it, and he and his band performed it the next day at the concert.

Johnny Cash at San Quentin was recorded live at San Quentin State Prison in California in February 1969, and released in June that year. It was the second live album from a prison by Cash, who had released At Folsom Prison the year before. The San Quentin album was produced by Bob Johnston, and went to #1 on the Billboard Top 200 Albums chart and Top Country Albums chart. The single from the LP, "A Boy Named Sue," was released in July 1969, and went to #1 on the Billboard Country Singles, and #2 on the Billboard Hot 100 Singles chart. Johnny Cash at San Quentin has been certified 3x Platinum by the Recording Industry Association of America. Personnel on the record were: Johnny Cash (lead vocals, acoustic guitar), June Carter Cash and the Carter Family (backing vocals), The Statler Brothers (backing vocals), Marshall Grant (bass), W.S. Holland (drums), Carl Perkins (electric guitar), and Bob Wootton (electric guitar). The iconic album cover photo was shot by Jim Marshall.

Johnny Cash was an American singer, songwriter, musician, and actor. He has sold more than 90 million records worldwide. He released 67 studio albums, 12 live albums, 102 compilation albums, four soundtrack albums, and 170 singles. Cash had 13 #1 singles in his career, and has won four Academy of Country Music Awards, one American Music Award, nine Country Music Association Awards, 17 Grammy Awards, and one MTV Video Music Award. He is a member of the Rock and Roll Hall of Fame, Country Music Hall of Fame, Gospel Music Hall of Fame, and Rockabilly Hall of Fame. Cash has won a Kennedy Center Honor, a National Medal of Arts, and a Grammy Lifetime Achievement Award, and has a star on the Hollywood Walk of Fame. Johnny Cash died in September 2003, four months after his wife June.

联系客服