JHVEPhoto

Shopify (NYSE:SHOP)’s shares have suffered a brutal decline of 73% from their all-time high as investors priced in slower post-pandemic growth for the e-Commerce company. However, I believe that Shopify has a very strong market position in the retail e-Commerce market with merchants that run small and medium-sized online stores and that this moat translates into significant pricing power for the company’s subscription plans. The e-Commerce company said last week that it will increase subscription plan prices for its merchant base which could result in a reinvigoration of Shopify’s top line growth. Although shares aren’t cheap, Shopify has significant recovery potential!

Shares of Shopify have seen a very sharp revaluation to the down-side after the pandemic and the company didn’t even give a revenue forecast for FY 2022 due to macroeconomic uncertainty. Shopify also announced that it would lay off 10% of its workforce last year as slowing growth forced the e-Commerce company to show more cost discipline and look for new revenue sources. Shopify has seen a major deceleration of its growth prospects in the last year, but this is about to change now.

Shopify announced in a blog post 5 days ago that it will increase its subscription prices for the Basic, Shopify, and Advanced plans which will take effect on April 23, 2023. Prices for monthly plans are set to go up by about 33% this year, potentially giving Shopify’s top line a nice lift going forward.

What makes the price hikes interesting for investors is that Shopify has invested heavily in the past to add new products and services to its platform which has helped create a moat for the e-Commerce company. Due to Shopify’s significant moat in the e-Commerce retail market and a lack of competition that offers a comparable product suite, I believe few merchants are going to respond to the firm’s subscription price increase by leaving the platform. The moat gives Shopify strong pricing power and the increase in plan prices could result in double-digit organic revenue growth going forward.

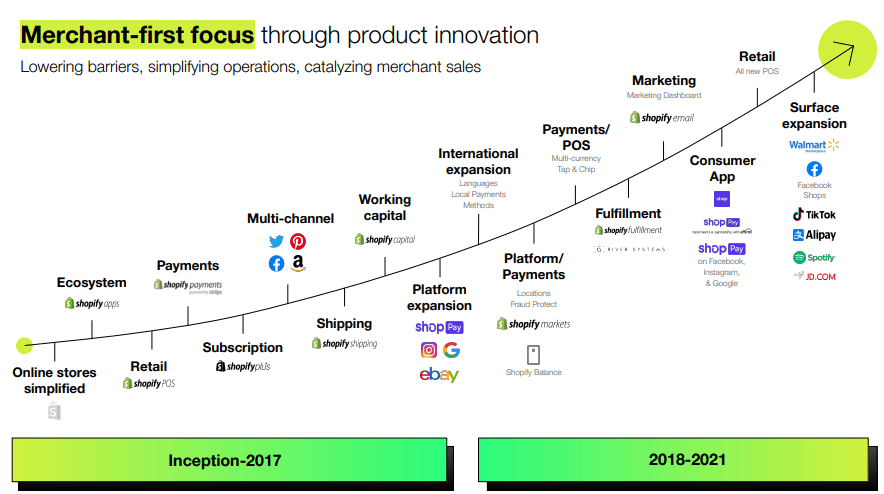

Shopify has heavily invested in the roll-out of new products and services since its inception, but especially since 2018 when the company added Payments services, fulfillment capacity and deeper analytics insights… all which have contributed to the creation of a merchant-centric business model. These value-added, non-subscription plan services are what will likely keep merchants on the Shopify platform, despite the increase in subscription prices.

Source: Shopify

What I like about the proposed changes in the pricing structure is that they support a part of Shopify’s business that has taken a bit of a backseat for the e-Commerce company in recent years. The real momentum for Shopify has been in Merchant Solutions which captures revenues from services that are ancillary to the subscription business. Services here include the use of Shopify’s payment gateway, Shopify Capital which helps with business funding, or Shopify Shipping. In all cases, these services complement Shopify’s basic offer of monthly subscription plans.

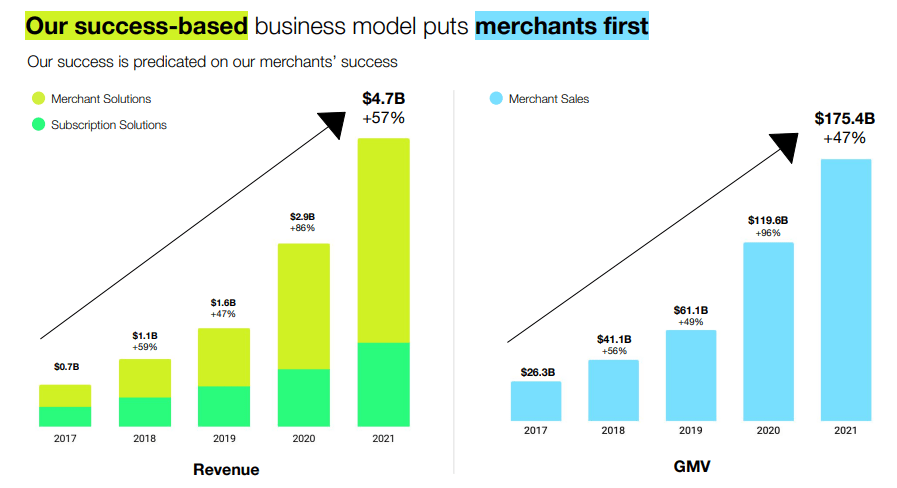

In the third-quarter, Shopify’s subscription revenues grew 12% year over year to $376.3M while Merchant Solutions grew at a rate of 26% year over year to $989.9M. So not only are Shopify’s Merchant Solutions growing a lot faster, but the revenue base is also 2.6 times larger than Subscription solutions.

Merchant Solutions have dominated Shopify’s business mix in the last couple of years…

Source: Shopify

With Shopify’s price increases set to take effect in April, I believe Subscription Solutions could grow into a $1.75B to $1.80B annual business compared to $1.5B today, showing a potential growth rate of 15-20%. Considering that many merchants don't have any real options to go to other e-Commerce companies with similarly broad product suites, Shopify is in a top position to grow its revenues organically.

Shopify has never really been cheap, and I do not expect that the e-Commerce company will be anytime soon. Shopify has seen enormous growth since its inception and the company has a dedicated and loyal customer base which adds to the moat-like characteristics of Shopify’s e-Commerce platform. For those reasons, I believe Shopify has considerable potential to grow its revenue base going forward and, possibly, much faster than estimates indicate.

The projection is for Shopify to grow its revenues to $8.37B in FY 2024, implying 26% year over year growth. But those estimates do not account for the potentially significant impact of subscription plan price increases. I believe it is possible for Shopify to grow consolidated revenues faster than the estimates currently indicate which could lead to an increase in the multiplier factor.

Currently, Shopify is valued at 7.6 X forward revenues, but the e-Commerce company was priced at more than double this multiplier factor last year. If Shopify can reinvigorate its revenues, I believe investors would be willing to reward the stock with a higher valuation factor.

The biggest commercial risk for Shopify is moderating top line growth as well as the potential (theoretically at least) that some of the merchants that are going to get hit by rising subscription prices will down-grade their subscription plans or not renew them altogether. However, merchants have very limited options to go elsewhere and Shopify’s impressive product suite surrounding subscription plans (all the products and services offered as part of Merchant Solutions) mark a strong incentive for merchants to accept the proposed subscription plan prices increases and stick with the Shopify platform nonetheless. A failure to revive top line growth would likely result in a lower valuation factor for shares of Shopify.

In a high-inflation world and in a market that has seen slowing revenue growth after the pandemic, I believe that the increase in subscription prices is a great move for Shopify to reinvigorate its top line growth. By raising subscription prices, Shopify is also showing the market that it has a way of spurring organic revenue growth in a segment that has not seen a whole lot of momentum (or attention) lately. I believe subscription price increases could result in 15-20% revenue growth in the subscription segment going forward. While not cheap, I believe a reinvigoration of Shopify’s revenue growth could result in a major upwards revaluation of the company’s shares in FY 2023!

联系客服