First, though nothing new, it shows the relatively small stock of longer dated securities and illustrates the ease at which the Fed can repress longer term interest rates and engineer short squeezes. The result has been the castration of the bond market vigilante and early grave for many hedge fund managers.

Second, the Fed holds over 40 percent of the Treasuries outstanding in several of the years in which they mature. In many of the specific maturities, the Fed owns up 60-70 percent of the total outstanding issue. The Fed had to “relax” its self imposed 35 percent limit on SOMA holdings of individual issues and included recently issued securities in order to execute its maturity extension program announced last September.

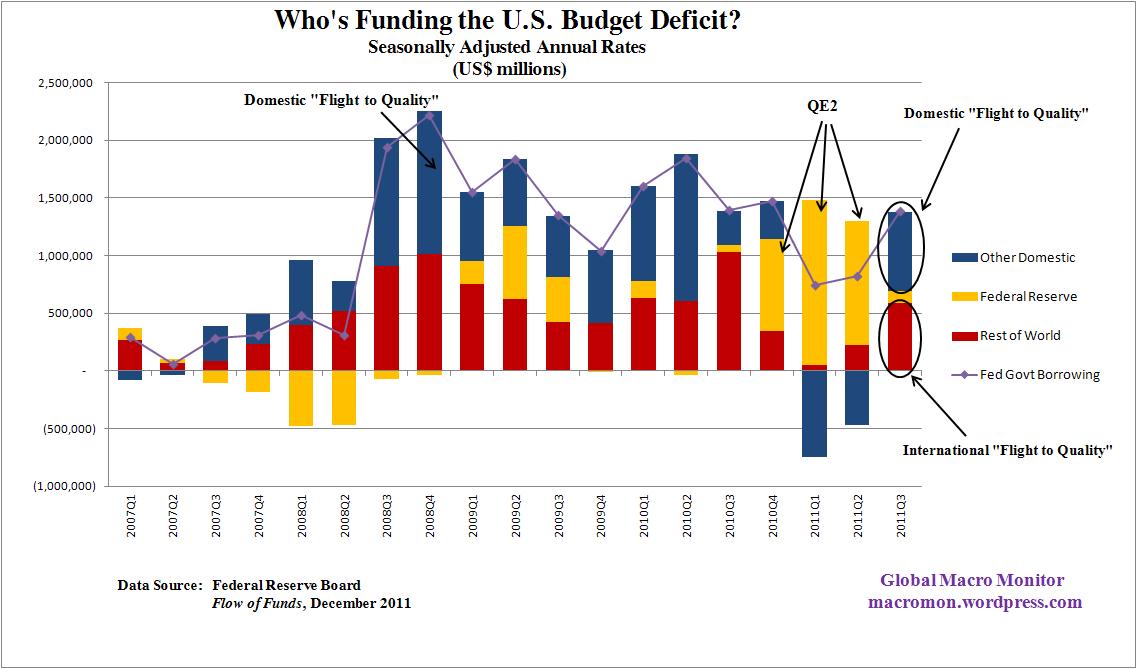

It’s going be interesting to see how longer-term interest rates behave as the economy regains some of its mojo and money comes out of the Treasury safe haven. The Fed has yet to fight the markets in its repression of long rates as Operation Twist has been riding the tail winds of positive market psychology and strong demand for safe havens due to Europe’s sovereign debt and banking crisis. See chart below.

As the issuance and stock of longer dated Treasuries increase with a larger structural U.S. budget deficit the Fed will need more firepower than just the interest earnings and roll off of maturing securities to keep rates from rising, in our opinion. They will need an even bigger bazooka if they are seen falling behind the curve on the economy or inflation. They will need a tactical nuke if the markets begin to lose confidence in the U.S. government’s fiscal and debt policies and starts to price credit risk. As the greatest QB in NFL history once said, “Confidence is a very fragile thing.”

No wonder there’s still talk of quanto easing and reassurance from the FOMC that interest rates will stay at “exceptionally low levels…at least through late 2014″ even as the stock market moves back to levels not seen since before the Lehman Crisis. Either stocks are wrong at pricing a better future than a U.S. monetary policy still in crisis mode or it will need more QE crack to keep the buzz alive and momentum intact.

We’re the first to admit nobody knows the future, most of all us, but we smell a potential fight or flight in the bond market, comrades. An Arab Spring in the bond pit, if you will. With oil prices north of $100 and rising rents, which is the largest component of the CPI, it is our sense the Fed better be able “to float like a butterfly and sting like a bee.”

We know it’s too early, but maybe this potential macro swan — rising interest rates and an emerging crisis of confidence in the Federal Reserve and the U.S. G’s fiscal and debt policies — has a fatter tail than currently perceived and should be on the radar. You never know, for sure, until you do, but then it’s too late. Thus, we will constantly remind ourselves of this in the new bull market in stocks — i.e., to make sure we panic before everyone else.

As they say in the ring, “Ladies and Gentleman, Let’s get ready to rumble!”

Click on charts to enlarge and for better resolution.